COVID

Recent headlines about the coronavirus have seen global stock markets decline for what is now the sixth straight day. And the question on everybody’s mind is: how much worse will this get? In times like these, it's critical for investors to maintain perspective and distinguish between how we react to world events in our everyday lives and how we respond in our financial lives.

In our everyday lives, it makes sense to heed expert advice on travel restrictions and take basic, sensible precautions. The same is true in our financial lives. When it comes to our investment portfolios, it often takes real discipline to avoid short-term panic. Investors today are bombarded by influential sources such as the financial media, pundits focused on short-term trading, and even friends and colleagues who may feel that the sky is falling. It can be difficult to distinguish between appropriate investment advice and knee-jerk reactions driven by market fear and panic. It's understandable that in these situations, some investors may be tempted to sell long-term investments and seek safety.

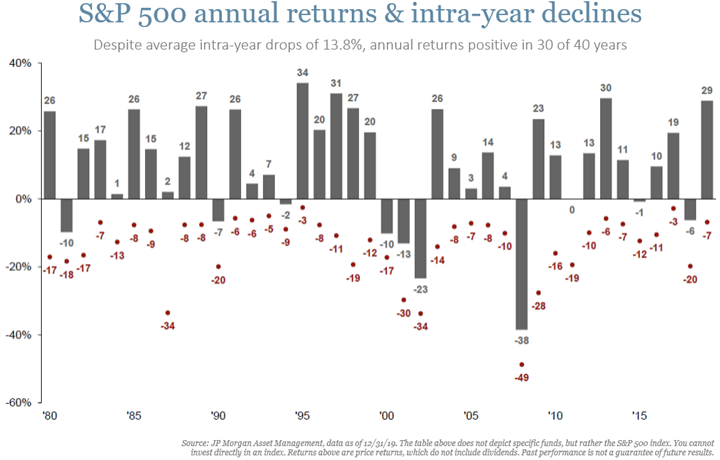

First, let’s acknowledge that with markets performing so well over the past year, a pullback was inevitable. Last year was impressively strong, with the S&P 500 up 31.5% (including dividends) for the full year 2019, and very little in the way of intra-year declines. The worst pullback in 2019 was a drop of 6.8% from the May 3rd peak, and it took 23 business days to occur. That compares to today’s pullback, which is now 10.6% (as of this writing) below the February 19th peak (in only 4.5 days). However, it’s important to note that markets have a long track record of becoming volatile – for one reason or another – and testing investors’ resolve. To put those numbers into perspective, the average intra-year drop is approximately 14% - and most of those years finish positive for the full year (see Figure 1).

FIGURE 1:

Secondly, let’s assess the current outbreak. While we would never downplay the human suffering element of this story, we believe it is key for investors to maintain appropriate perspective, and to that extent, we feel there are two worthy statistics which aren’t receiving as much attention: 1) the fatality rate is much smaller than comparable outbreaks, and 2) total active cases have been declining for 10 days. According to the World Economic Forum, the fatality rate of the coronavirus is about 2%, which compares to 10% for SARS (2003) and approximately 35% for MERS (2012-2013). Additionally, news outlets continue to update the number of people who have been infected (82,588 as of this writing), which is a cumulative statistic that will never go lower. We believe it is more relevant to track the total number of active cases – which subtracts the number of resolved cases (both deaths and recoveries) – to give us better context on the number of people currently battling the virus. According to Worldometer, which aggregates statistics from health agencies across the world, eleven days ago (2/17/20) that figure peaked at 58,747, and it is now 21% lower (at 46,429 currently). It is also notable that while the coronavirus has infected what seems like a large number of people across the world, in the US alone during the 2019-2020 flu season there were at least 15 million flu illnesses, 140,000 hospitalizations and 8,200 deaths, according to the World Health Organization.

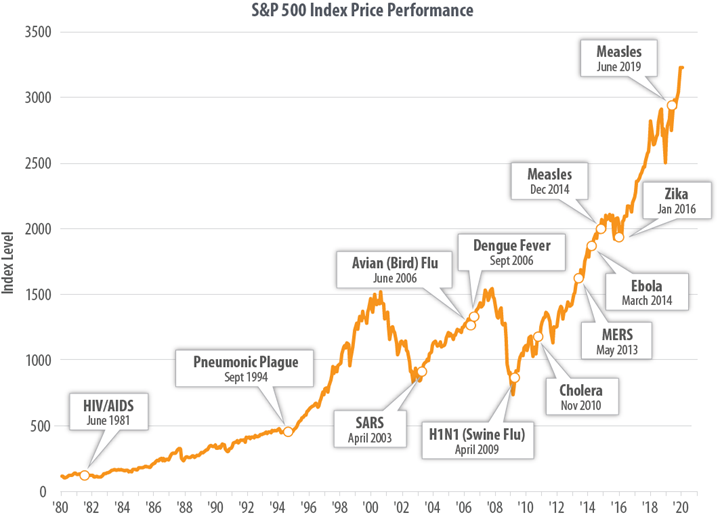

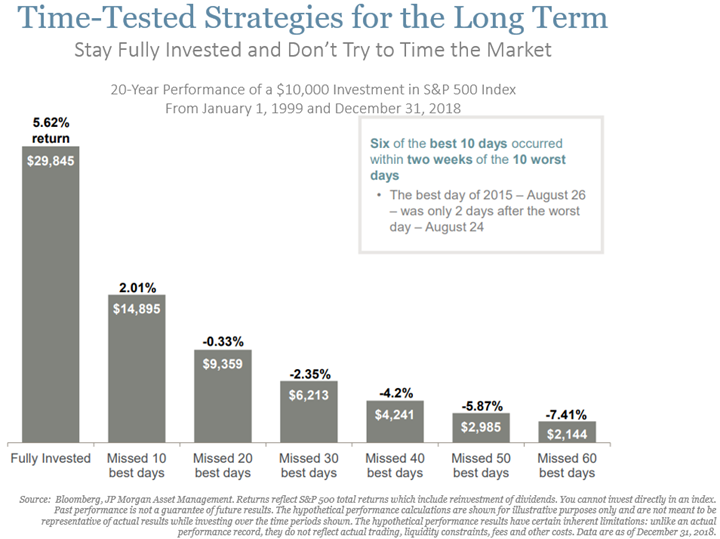

Lastly, we remind investors that trying to time the market by selling stocks and “waiting until the dust settles” is a very difficult endeavor – one that usually results in missing the best-return days, which tend to cluster around the worst-return days (see Figure 2 below). While it is unclear when the coronavirus will be fully contained, we would note the following positives: 1) technology, medicine, and communications allow much faster and better coordinated mobilization efforts against outbreaks than ever before, 2) health scares rarely cause anything more than temporary market dislocations, 3) full-on recessions are usually caused by excessive Fed tightening or extreme valuations, and 4) the US consumer (the economic engine of the US) remains in good shape, which portends well for the US economy. Achieving financial goals is a long-term proposition. For that reason, we advise investors to filter out the short-term noise and focus on the long run, while taking advantage of opportunities to rebalance and harvest losses where appropriate for tax purposes. While it’s impossible to know for sure, we are inclined to believe that like those infections in the past, this too shall pass (see Figure 3 below).

FIGURE 2:

FIGURE 3: